Just like everything in life, personal circumstances are always changing and sometimes that affects financial health. Changes in your personal circumstances may include affecting your ability to make payments on your mortgage. Your mortgage is already affected, and you are at risk of a mortgage default in some instances.

Getting a notice of mortgage default is actually pretty stressful, but by knowing what to do you will easily deal with such a serious problem. Here below is the detailed step-by-step procedure you may take after getting such a notice that will prepare you with the best practice and insight into securing your future.

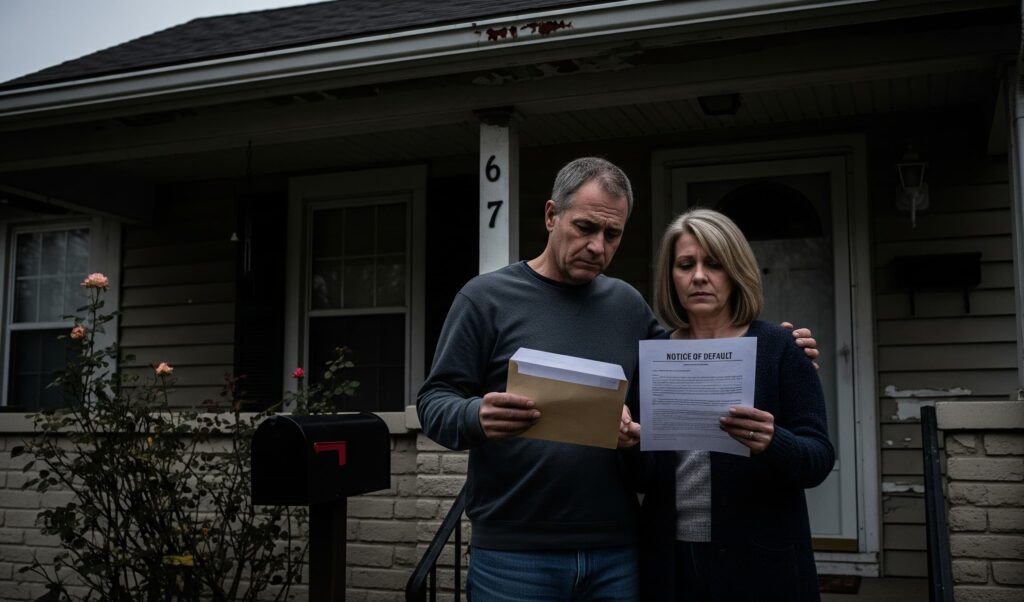

A notice of default is a public notice filed with a court or local recording office as a request to start the foreclosure process. A mortgage lender or service can file this notice if there are four months (120 days) of defaulted payments.

Notice of mortgage default is the communication received from your lender indicating you have failed to comply with the terms of your mortgage agreement. This is normally done after several payments that are missed and leads up to the foreclosure case, which might be undertaken against you in case no action is taken on time.

The notice typically contains what is known as the notice of default and right to cure, an element that lets you know what that particular default is and when to fix it.

Once you receive a mortgage default notice, the following steps need to be taken immediately:

The following are possible steps you could undertake to handle your mortgage default:

Repayment Plan: You could get in touch with your lender and then agree to a feasible schedule for the repayment.

Loan Modification: Alter the existing terms of your loan so that you can conveniently pay.

Refinancing: Get a new, better loan to replace or substitute your existing mortgage loan.

Selling Your House: If you cannot make the payments and owning remains too heavy, selling can be a good option.

Issuance of notice to default on a loan puts you in a serious vulnerable position. Foreclosure looms large. You also need to know your rights in law:

At Redhead Home Properties, they understand that facing mortgage difficulties can be stressful. Their team works to provide tailored solutions securing your home and future. Whether you are looking to refinance or find a new property that better suits your budget, Redhead Home Properties is here to help. Visit them at Redhead Home Properties to learn more and get the support you deserve today.

Receiving a notice of mortgage default does not define the end of the road. With proper guidance and support, one can get through this difficult time and secure their future financially. It is more about taking informed action and exploring all avenues for the best solution to your situation.

Yes, in case a party believes that the notice received to him is wrong or wrongly presented, then he ought to dispute the notice with all documents relevant to his case and seek for advice from a legal advisor to help appeal for him.

A loan default notice will drastically reduce your credit score, which will also have an impact on further loan opportunities and better interest rates. Or maybe you will get a letter of credit default.

Yes, you can sell your house, and it might be a wise choice if you do not want to go through foreclosure. You can consult real estate agents who can advise you about the options.

I'm Zoey Wilson. I am a professional content writer with 5+ years of experience creating research-based, informative, and explicit content to help readers understand the topic, form opinions, and implement processes. My content work combines deep market knowledge and a practical approach, giving you a real picture of today's industry landscape with reliable insights.